How to Calculate Gross Profit Using LIFO (Step-by-Step with Examples)

To calculate gross profit using LIFO, subtract your LIFO-based cost of goods sold (COGS) from total sales revenue using the formula: Gross Profit = Revenue – COGS (LIFO). The result is almost always lower than what you’d get under FIFO, and that difference matters a lot when it comes to taxes.

Having worked with hundreds of eCommerce and small business owners on financial reporting and inventory decisions, we’ve seen this one concept cause more confusion than almost anything else in accounting. Most guides show you the formula and stop there. What they skip is why the number changes depending on how you track inventory, and what it actually costs you if you get it wrong.

This post walks through the full step-by-step calculation, a worked example with real numbers, and a clear comparison of LIFO vs FIFO so you can see the difference in practice.

What Is the LIFO Method? (And Why It Affects Gross Profit)

LIFO stands for Last In, First Out. It’s an inventory valuation method that assumes the most recently purchased stock is what gets sold first. That assumption might sound simple. However, it has a direct impact on the amount of profit you report and the amount of tax you owe.

Here’s the thing: LIFO doesn’t describe how your physical inventory actually moves. It’s purely an accounting choice. You can sell products in any order you want. LIFO only determines which cost layer gets assigned to the units you’ve sold when you calculate your COGS.

How LIFO Works: The Core Assumption

Think of a stack of products arriving in your warehouse. Every new shipment goes on top. Under LIFO, when a customer makes a purchase, the cost is pulled from the top of the stack first, which means the most recent purchase price is used.

If your supplier charges more each month (which is common during inflation), those newer, higher costs hit your COGS first. Higher COGS means lower gross profit. Lower gross profit means lower taxable income. That tax angle is exactly why many US businesses choose LIFO.

Worth knowing: LIFO is only permitted under US Generally Accepted Accounting Principles (GAAP). International Financial Reporting Standards (IFRS) ban it outright, so if you operate globally or plan to, LIFO is off the table.

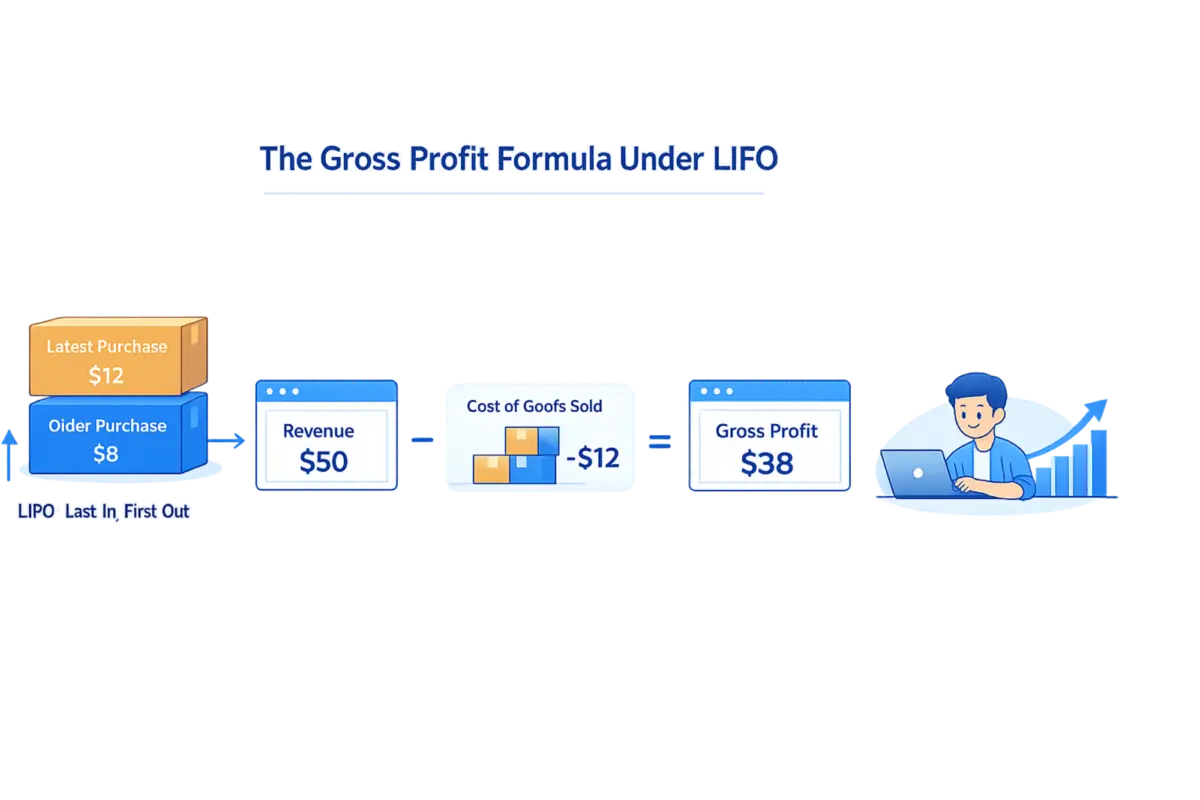

The Gross Profit Formula Under LIFO

The formula itself never changes:

Gross Profit = Revenue – Cost of Goods Sold (COGS)

What changes under LIFO is how you calculate COGS. Once you have your LIFO-based COGS number, the rest is straightforward subtraction. The tricky part is building that COGS figure correctly, which is what the next section covers.

How to Calculate Gross Profit Using LIFO: Step by Step

Here’s the full process. These steps work for any business selling physical products, whether you run a retail shop, a WooCommerce store, or a small manufacturing operation.

- Step 1: Identify your sales revenue for the period: This is the total amount your customers paid. If you sold 200 units at $50 each, your revenue is $10,000. Revenue does not change based on your inventory method.

- Step 2: List your inventory purchases in chronological order: Write down every batch of inventory you bought during the period, including how many units and what you paid per unit. Label each by date so you can identify the most recent purchases.

- Step 3: Calculate how many units were sold: Under the periodic LIFO method, you add up all sales for the period first, then assign costs. Under the perpetual method, you assign costs at the time of each sale. More on that difference in the next section.

- Step 4: Assign costs to sold units starting with the most recent purchase: Work backwards through your purchase list. Use up the newest batch first. If that batch doesn’t cover all units sold, move to the next most recent batch, and so on.

- Step 5: Add up the total cost assigned to sold units: That is your COGS.

- Step 6: Subtract COGS from revenue: Gross Profit = Revenue – COGS (LIFO)

Worked Example: A Small Business Selling Phone Accessories

Say you run a small business selling phone cases. Here’s your inventory for the quarter:

- January: Bought 100 units at $5.00 each = $500

- March: Bought 100 units at $7.00 each = $700

- September: Bought 100 units at $9.00 each = $900

Total goods available: 300 units at a combined cost of $2,100

During the quarter, you sold 200 units at $15.00 each.

Revenue: 200 x $15 = $3,000

Under LIFO, you assign the most recent costs first:

- 100 units from September at $9.00 = $900

- 100 units from March at $7.00 = $700

- COGS (LIFO) = $1,600

Gross Profit (LIFO) = $3,000 – $1,600 = $1,400

Your ending inventory is 100 units from January at $5.00 each = $500.

LIFO vs FIFO: How the Gross Profit Numbers Differ

Same business, same sales, same purchase prices. Let’s run the same example under FIFO and see what changes.

Under FIFO, you sell the oldest inventory first:

- 100 units from January at $5.00 = $500

- 100 units from March at $7.00 = $700

- COGS (FIFO) = $1,200

Gross Profit (FIFO) = $3,000 – $1,200 = $1,800

Here’s the comparison side by side:

| LIFO | FIFO | |

|---|---|---|

| Revenue | $3,000 | $3,000 |

| COGS | $1,600 | $1,200 |

| Gross Profit | $1,400 | $1,800 |

| Ending Inventory | $500 | $900 |

The difference is $400 in gross profit. That’s money that appears as profit under FIFO but gets included into COGS under LIFO. In most tax brackets, that $400 difference saves a meaningful amount in taxes. As the US Chamber of Commerce notes, in a rising-cost environment, LIFO results in lower gross profit and lower taxable income, which is the primary reason businesses choose it.

This gap grows larger as inflation increases and as your inventory volumes scale up. A business buying $500,000 in inventory annually is looking at potentially tens of thousands in tax savings under LIFO compared to FIFO.

Here is the detailed guide on how to calculate gross profit using the FIFO method, which will give you a deep understanding of the FIFO inventory method with examples.

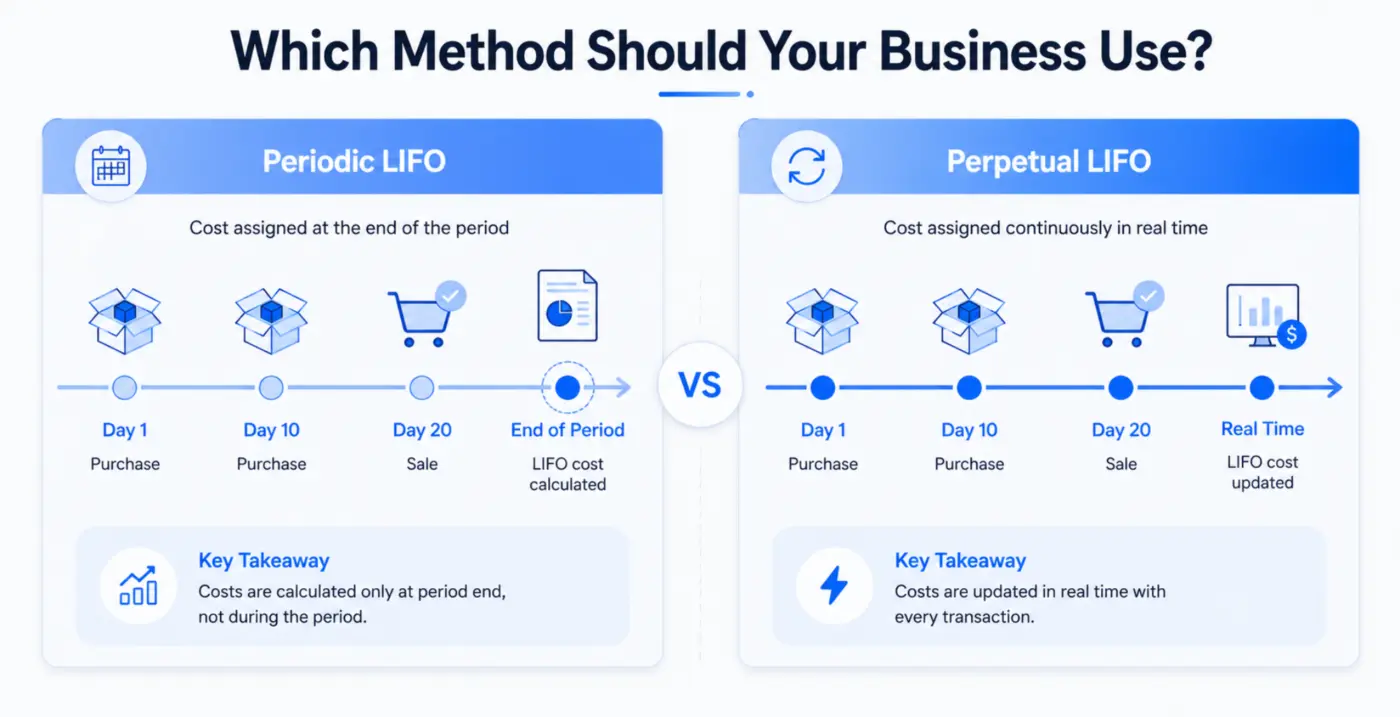

Periodic LIFO vs Perpetual LIFO: Why You Get Different Numbers

This is the part most guides skip entirely. And it’s the part that causes the most confusion when your accountant’s numbers don’t match what you calculated yourself.

There are two ways to track inventory: periodic and perpetual. The method you use determines when you assign LIFO costs, and that timing changes your COGS and your gross profit.

Periodic LIFO Gross Profit Calculation

Under the periodic method, you only calculate inventory at the end of the period. You add up everything sold across the whole quarter or year, then work backwards from your most recent purchase to assign costs.

This means the absolute newest purchase prices always hit COGS first, regardless of when during the period sales actually happened. The result is usually the highest possible COGS under LIFO, and therefore the lowest gross profit.

Perpetual LIFO Gross Profit Calculation

Under the perpetual method, you assign costs every time a sale happens, using only the inventory that’s on hand at that moment. If a sale happens in January before a new shipment arrives in March, those cheaper January costs go into COGS for that sale.

The result: perpetual LIFO often produces slightly lower COGS and slightly higher gross profit than periodic LIFO for the same data set. Not by a huge amount, but enough to matter on large volumes.

As AccountingTools explains, perpetual LIFO is now far more common because most businesses track inventory digitally and update records in real time.

Which Method Should Your Business Use?

Most small businesses using accounting software, a POS system, or an eCommerce platform are already on perpetual inventory by default. Their systems log every sale and update inventory counts automatically. If that’s you, you’re using perpetual LIFO whether you knew it or not.

Periodic inventory tends to suit very small businesses doing manual counts monthly or quarterly. The calculation is simpler but less precise.

What LIFO Gross Profit Actually Means for Your Tax Bill

A lower gross profit under LIFO isn’t a bad thing. For most profitable businesses, it’s the whole point. Lower gross profit flows through to lower net income, which means lower taxable income, which means a smaller tax bill.

The LIFO Conformity Rule

Before you decide to use LIFO for tax purposes, there’s a rule you need to know about. The IRS requires that if you use LIFO for your tax return, you must also use it for your financial statements. You cannot show LIFO on your taxes and FIFO on your reports to lenders or investors.

This is called the LIFO conformity rule, and it matters because lower reported profits can affect loan approvals, investor perceptions, and business valuation. Some business owners who genuinely benefit from LIFO on taxes hesitate because they don’t want their profit margins to look lower on paper. That’s a real trade-off, and it’s worth discussing with an accountant before you elect LIFO.

LIFO Reserve and What It Reveals

The LIFO reserve is the difference between what your inventory would be worth under FIFO and what it’s actually reported at under LIFO. Most US GAAP companies that use LIFO are required to show this figure in their financial statements.

LIFO Reserve = FIFO Inventory Value – LIFO Inventory Value

A large LIFO reserve means the method has saved you a lot in taxes over time. It also means there’s a hidden tax liability sitting on your balance sheet. If you ever sell off that inventory or switch away from LIFO, the IRS collects.

LIFO Liquidation: The Risk No One Warns You About

This is the part that trips people up. If you sell more inventory than you buy in a given period, you start dipping into older, cheaper inventory layers. Under LIFO, those older, lower-cost units get assigned to COGS. Lower COGS means higher gross profit than usual, which means a higher tax bill.

This is called LIFO liquidation, and it creates what accountants sometimes call “phantom profits.” Your gross profit looks artificially high, not because your business is doing better, but because your inventory levels dropped. It’s a temporary and unsustainable spike.

If your industry is seasonal or you’re managing cash flow tightly, keeping an eye on your inventory levels relative to your LIFO cost layers is worth the time. A sudden restocking at higher prices after a liquidation event can create a messy accounting picture if you’re not tracking it. Understanding how to value your business’s assets accurately is part of avoiding this kind of surprise.

When LIFO Makes Sense (And When It Does Not)

LIFO is not the right choice for every business. Here’s a practical breakdown.

LIFO works well when:

- Your product costs are rising steadily (due to inflation, supplier increases, or tariffs)

- You carry large volumes of inventory, and the tax savings are material

- You are a US-based business reporting under GAAP

- You do not need to show maximum profitability on paper for lenders or investors

In 2026, with ongoing inflation and significant tariff increases affecting imported goods, businesses dealing in electronics, auto parts, clothing, and general merchandise are finding LIFO more valuable than in previous years. According to CBIZ, the method is gaining renewed attention specifically because tariff-driven cost increases are exactly the scenario where LIFO’s tax deferral works best.

LIFO is a poor fit when:

- Your products are perishable or time-sensitive (food, pharmaceuticals). Older inventory sitting on the balance sheet is not just a number problem. It’s a real operational risk.

- You report under IFRS or operate internationally. LIFO is banned under IFRS, which means multinational businesses or those considering foreign listings need a different approach.

- You want to show higher profit margins to attract investors or secure financing. The conformity rule means lower profits on paper if you go LIFO.

- Your inventory costs are falling. In a deflationary environment, LIFO actually increases gross profit, which is the opposite of what most businesses want.

Understanding how inventory decisions affect your overall numbers is connected to the broader question of how to calculate customer lifetime value in eCommerce. Both come down to knowing exactly which costs are hitting your margins and when.

Conclusion

Calculating gross profit using LIFO comes down to three things: identifying your cost layers in reverse chronological order, assigning the most recent costs to sold units, and then subtracting that total from revenue. The formula is simple. What takes more care is choosing between periodic and perpetual tracking, understanding the conformity rule, and watching for LIFO liquidation events that can inflate your reported profit unexpectedly.

LIFO is not a trick or a shortcut. It’s a legitimate, IRS-sanctioned inventory method that reflects current costs more accurately in an inflationary environment, and it genuinely reduces your tax bill when used correctly. The key is using it consistently, disclosing your LIFO reserve, and not letting inventory levels drop to the point where older cost layers bleed into your COGS.

If you run an eCommerce business or physical product store and want sharper visibility into how your product costs affect margins and business value, explore our eCommerce resources at DevDiggers for practical guidance built for product sellers.

Frequently Asked Questions

Q1. Does LIFO always result in lower gross profit than FIFO?

Not always, but it does in most situations businesses face. When inventory costs are rising, which is the case during inflation, LIFO assigns the higher recent costs to COGS first. That increases COGS and reduces gross profit compared to FIFO. In a deflationary environment where prices are falling, the relationship reverses: LIFO would produce a higher gross profit than FIFO.

Q2. Can I use LIFO for taxes but FIFO for my financial statements?

No. The IRS conformity rule requires that if you elect LIFO for tax reporting, you must also use LIFO for your primary financial statements. You can add a supplemental FIFO-based disclosure, but LIFO must be the basis of your reported figures. Violating this rule can result in the IRS ending your LIFO election.

Q3. What happens to gross profit if I switch from FIFO to LIFO?

Your gross profit will typically drop in the first year of the switch, because you are now assigning higher recent costs to COGS instead of lower historical ones. That lower gross profit reduces taxable income, which is usually the reason for switching. The IRS requires you to file Form 970 to officially elect LIFO, and you must apply it consistently going forward.

Q4. Is LIFO allowed outside the United States?

No. LIFO is permitted only under US GAAP. International Financial Reporting Standards (IFRS), which govern accounting in most other countries, explicitly prohibit LIFO. Businesses operating internationally or listed on foreign exchanges cannot use LIFO for those reporting purposes.

Q5. How does LIFO liquidation affect gross profit?

When a business sells more inventory than it purchases in a period, it dips into older, cheaper cost layers. Under LIFO, those lower costs flow into COGS, which reduces COGS and temporarily increases gross profit. This is called LIFO liquidation. The higher gross profit looks good on paper, but is not sustainable and often triggers a higher-than-expected tax bill for that period.

Q6. Does my choice of a periodic vs continuous inventory system change my LIFO gross profit?

Yes, it can. Periodic LIFO assigns the very latest costs to COGS at the end of the period, typically producing the highest COGS and lowest gross profit. Perpetual LIFO assigns costs at the time of each sale, using only the inventory available at that moment, which can result in slightly lower COGS and higher gross profit for the same data set. For most businesses using modern accounting or eCommerce software, perpetual tracking is the default.

Kartika Musle

Kartika Musle is a tech writer at DevDiggers covering WooCommerce features, web design, and development security. Her articles translate technically dense subjects into guides that a non-developer can follow without losing the detail that matters, drawing on a background that touches both design and development.

Join thousands of readers getting smarter every week.

Leave a Reply